What is the Price-Free Cash Flow (P/FCF) Ratio?

The price-free cash flow (P/FCF) ratio is a valuation ratio that compares a company’s share price with its free cash flow per share. It is the inverse of the free cash flow yield.

How to Calculate the P/FCF Ratio

The P/FCF ratio is calculated by dividing the current market share price by the free cash flow per share of the current reporting period.

A publicly traded company’s market share price is readily found online, and the free cash flow per share can either be calculated, or can often be found on a company’s cash flow statement.

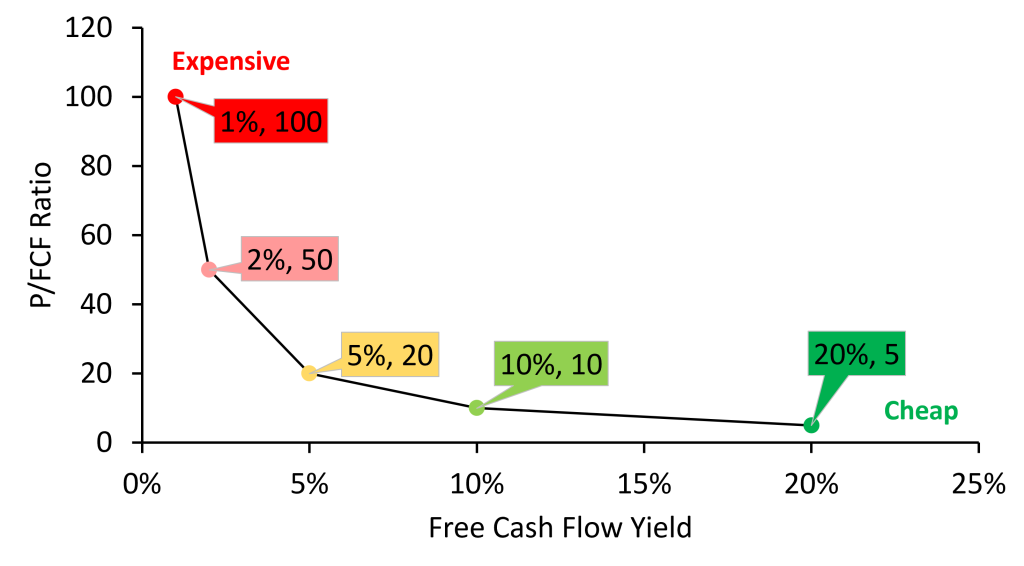

How to Interpret the P/FCF Ratio

A low P/FCF ratio such as 5, which corresponds to a free cash flow yield of 20%, suggests that a company’s shares are cheap.

A high P/FCF ratio such as 100, which corresponds to a free cash flow yield of 1%, suggests that shares are expensive.

Limitations of the P/FCF Ratio

The price-free cash flow (P/FCF) ratio as a relative valuation measure has certain limitations which need to be considered when evaluating whether a company’s shares are cheap or not.

1. A company must have positive free cash flow.

If a company shows negative free cash flow, the P/FCF ratio is not useful. This makes the P/FCF more useful for established, more mature businesses that achieve report positive free cash flow, and not as useful for younger companies that are more likely to show negative free cash flow. For younger companies, the price-sales (P/S) ratio is more useful as a relative valuation measure.

2. The P/FCF ratio may be overstating cheapness.

While a low P/FCF ratio suggests that a stock is cheap, it is not necessarily a reason to buy the stock. The market might be factoring in expectations of future poor performance of the stock, justifying the low price. On the other hand, the stock might actually be cheap due to mispricing of the market.

3. The P/FCF ratio may be understating cheapness.

A company with a high P/FCF ratio suggests that the stock is expensive. A company might achieve low earnings by investing heavily into expenses that build out an economic moat to ensure profitability in the future, possibly justifying the higher price.

For these reasons, a more suitable measure would be the PEG ratio, which factors in not only the P/E ratio, but the earnings growth rate.